Many people didn’t expect their Medicare costs to change this year—but for some beneficiaries, 2026 has already brought higher premiums. Even if your health hasn’t changed, your monthly costs can increase based on income alone. If you’ve noticed a jump in what you’re paying, understanding Medicare premiums increase due to IRMAA in 2026 can help explain what’s happening and what you can do next.

Skyline Benefit is an independent Medicare insurance broker helping individuals nationwide understand Medicare costs, review income changes, and make informed decisions about their coverage—at no extra cost.

What Is IRMAA and Why Is It Affecting Medicare Costs in 2026?

IRMAA (Income-Related Monthly Adjustment Amount) is an extra charge added to your Medicare Part B and Part D premiums if your income is above certain thresholds.

It’s not based on your health or how often you use care—it’s based strictly on your income.

That’s why two people with the same coverage can pay very different amounts.

Why Are Medicare Premiums Higher in 2026 for Some People?

The increase many people are seeing in 2026 comes down to how Medicare calculates income.

Your current premiums are based on your income from about two years ago—typically your 2024 tax return.

So even if your income has already dropped, Medicare may still be charging you based on what you earned back then.

This is the main reason behind the Medicare premiums increase due to IRMAA in 2026 that many beneficiaries are now experiencing.

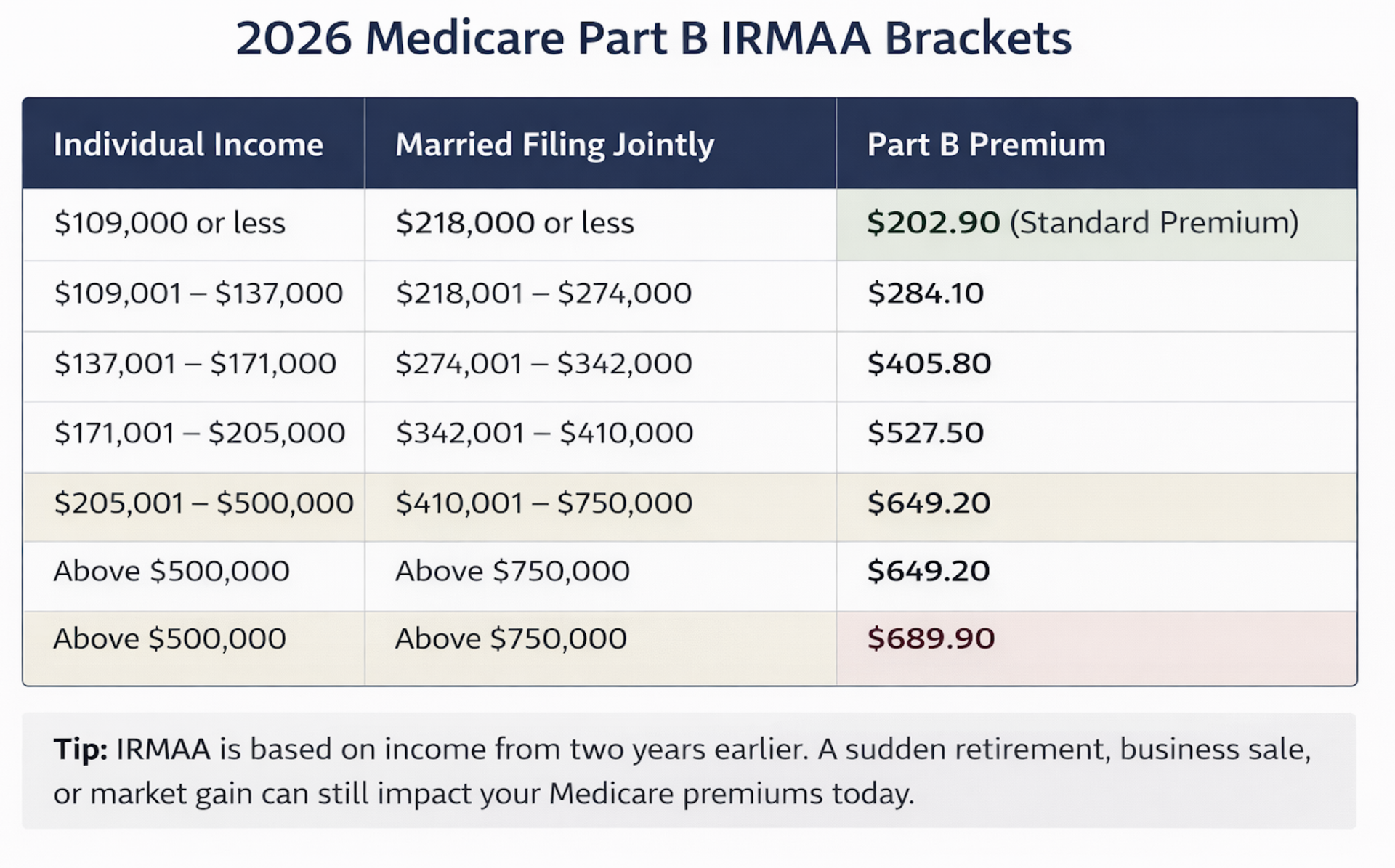

What Income Triggers IRMAA in 2026?

IRMAA applies once your income exceeds certain limits.

Your income is measured using Modified Adjusted Gross Income (MAGI), which may include:

- Wages or self-employment income

- Investment income

- Capital gains

- Rental income

The higher your income, the higher your IRMAA adjustment—and the more you’ll pay each month.

How Much More Are People Paying in 2026?

For many beneficiaries, IRMAA adds a noticeable increase to monthly Medicare costs.

This can include:

- Higher Part B premiums

- Additional charges for Part D prescription coverage

Depending on your income level, this increase can add up to hundreds of dollars per month—and for some individuals, even more.

Does IRMAA Affect Medicare Advantage Plans?

Yes—indirectly.

Even if you have a Medicare Advantage plan, you still must pay your Part B premium. If IRMAA applies, that premium will still be higher.

IRMAA also affects Part D costs, whether your drug coverage is standalone or included in your Advantage plan.

Can You Reduce IRMAA If Your Income Has Dropped?

Yes—and this is where many people miss an opportunity.

If your income has changed due to a life event—like retirement—you may be able to request a reassessment.

This is done using Form SSA-44.

In many cases, people who take this step are able to significantly reduce what they’re paying—especially when their current income no longer reflects past earnings.

What Life Events Can Help Lower IRMAA?

You may qualify for a reduction if your income dropped due to:

- Retirement

- Work reduction

- Loss of income-producing property

- Divorce or death of a spouse

If one of these applies, your current premiums may not accurately reflect your financial situation.

What Should You Do If Your Medicare Premiums Increased in 2026?

If you’ve already noticed higher premiums this year, start by reviewing:

- Your current income vs. past income

- Whether a life-changing event has occurred

- Whether your premiums still reflect outdated earnings

If your situation has changed, you may not have to continue paying at the current level.

Need Help Understanding Medicare Premiums Increase Due to IRMAA in 2026?

Skyline Benefit is here to help you understand Medicare premiums increase due to IRMAA in 2026, review your income situation, and explore ways to reduce your costs—at no extra cost.

Call us at: (714) 888-5112